What Every Transaction Can Tell You About Your Customer

Your transaction data already captures customer behaviour, lifetime value, and future spending patterns. The question is whether you're using it to move from anonymous payments and basic reports to business growth and identified, personalised customer relationships.

Your till processes hundreds, perhaps thousands, of transactions each week. Payment accepted, receipt printed, next customer. But what if each of those transactions was actually telling you a story about who that customer is, what they value, and how much they'll spend with you over the next three years?

Most retailers treat transaction data as an accounting necessity. The payment clears, inventory adjusts, revenue gets recorded, and the system moves on. Yet sitting in your payment infrastructure is detailed intelligence about customer behaviour, purchase patterns, and future value that you're barely using. You've been collecting the raw material for sophisticated customer understanding all along. The question is whether you're doing anything with it beyond monthly sales reports.

What Your Transactions Actually Capture

That £32.50 transaction from Tuesday morning contains far more information than the total amount. Embedded in every payment are contextual signals that reveal how customers behave, what they value, and what they're likely to do next.

Where they shop tells you whether customers prefer your high street location for quick lunch purchases or drive to your retail park store for bigger weekly shops. In multi-site operations, this cross-location behaviour reveals distinct needs and occasions. The customer popping into your Covent Garden café on weekday mornings has different requirements from the same person visiting your Clapham location on Saturday afternoons.

When they shop exposes patterns that monthly averages completely obscure. Some customers are religiously there on Saturday mornings. Others make quick convenience purchases on Tuesday evenings. Your lunchtime transactions look nothing like your evening baskets in both composition and value. Tesco pioneered this analysis decades ago, analysing transaction timing patterns to understand customer behaviour, but your specific temporal patterns matter more than industry benchmarks.

How they shop increasingly varies by channel. The customer who browses your website but always completes purchases in-store behaves fundamentally differently from the purely digital shopper. Understanding these preferences enables you to meet customers where they actually want to transact rather than forcing them into channels that suit your operations.

What they buy together reveals natural product affinities that demographic assumptions never would. When someone buying organic vegetables consistently adds premium coffee and sourdough, that's a behavioural segment announcing itself through actual purchases. These basket associations inform everything from store layouts to targeted promotions, but only if you're paying attention to the patterns.

This contextual data already flows through your payment systems. You're capturing it whether you analyse it or not. The intelligence gap isn't technical capability, it's analytical intent.

Understanding the Past: What Your Customers Have Done

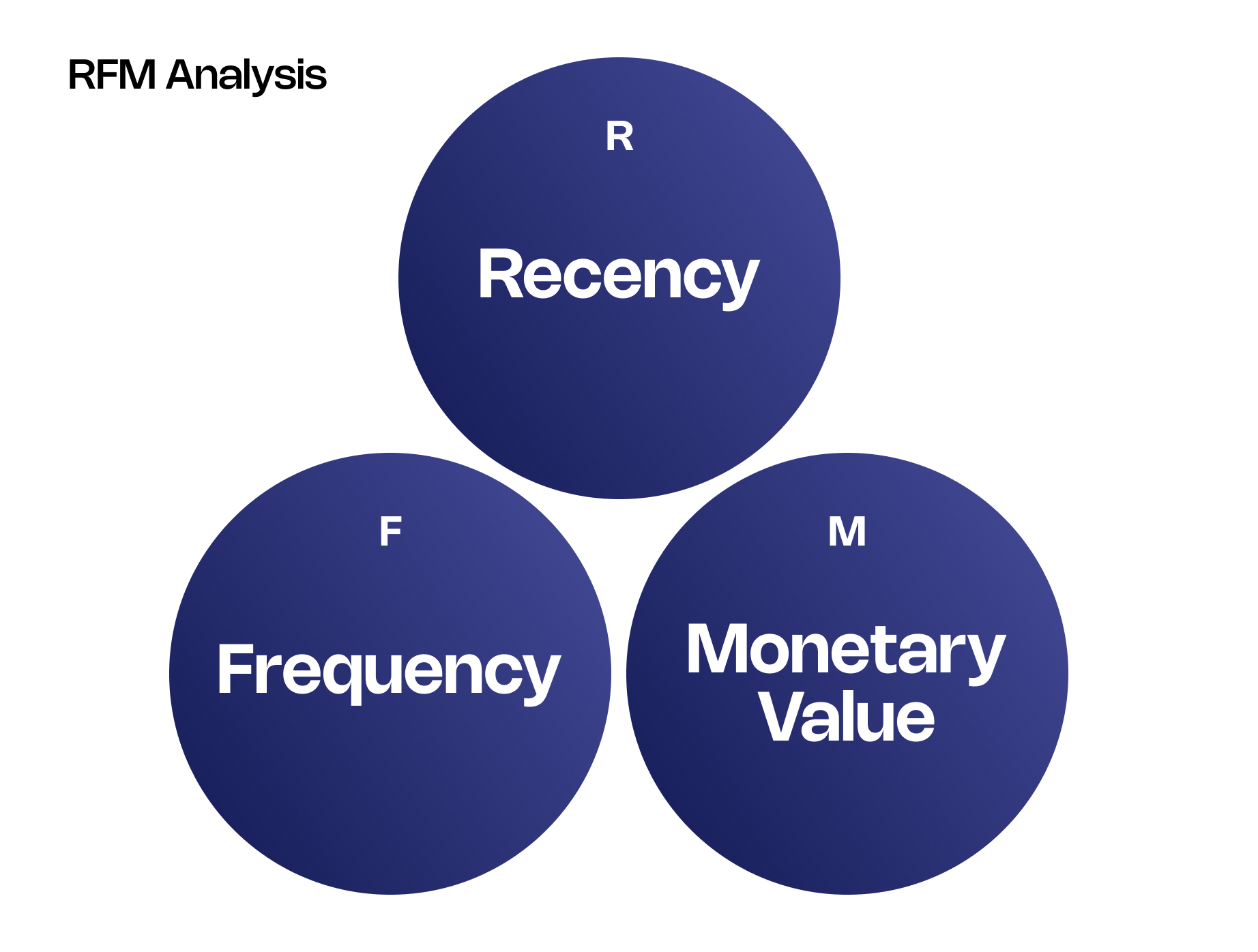

Before you can predict what customers will do, you need to understand what they've already done. This is where RFM analysis proves its worth. It's a framework that's existed since the 1990s, survived every retail trend since, and remains relevant because it captures the fundamentals of customer behaviour.

- Recency answers when they last purchased. A customer who bought yesterday is fundamentally different from one whose last visit was six months ago, regardless of how much they've historically spent. Recent purchasers are statistically far more likely to purchase again. Recency deteriorates over time, and in competitive retail markets, that deterioration happens faster than most merchants assume. By the time a previously regular customer hasn't visited in three months, they've likely shifted their spend elsewhere. You need to know this whilst there's still time to intervene.

- Frequency reveals how often they purchase. Someone transacting weekly demonstrates materially different engagement than a quarterly visitor. High frequency typically signals that you've become habitual for them, which provides resilience against competitive pressure. For grocery and hospitality particularly, frequency is the clearest indicator of whether you're a default choice or an occasional option. As an example, Sainsbury's Nectar programme tracks frequency patterns to reward customers based on how often they shop, using visit regularity as a primary signal for targeted engagement.

- Monetary value shows how much they spend. But here's where it gets interesting: a customer spending £200 once looks similar to someone spending £50 across four visits from a revenue perspective, but they represent entirely different relationships and future potential. High transaction values without frequency suggest occasional big-ticket purchases. Lower values with high frequency indicate habitual, sticky customers. Both have value, but very different kinds.

These three metrics combine to create segments with distinct characteristics. Someone scoring high across all three dimensions represents your most valuable current relationship. Low scores across the board signal customers who've already churned or were never truly engaged. The real intelligence emerges in the segments between these extremes: high frequency but low monetary value might indicate price-sensitive loyalty that's vulnerable to competitive discounting, whilst high monetary value with declining frequency suggests a previously valuable customer at risk of defection.

But RFM only tells you what's happened. It doesn't tell you what comes next.

Predicting the Future: What Your Customers Will Do

Customer Lifetime Value shifts your perspective from backward to forward. Whilst RFM describes historical behaviour, CLV predicts future profit. This transition from reporting to prediction represents the critical step from transaction data to transaction intelligence.

CLV quantifies the total profit a customer will generate over their entire relationship with your business. It takes your RFM segments and assigns them actual financial value, enabling precise decisions about how much to spend acquiring similar customers, how much to invest retaining existing ones, and where to allocate resources for maximum return.

The basic calculation requires three inputs. Average transaction value establishes baseline spending per visit. Purchase frequency determines how often those transactions occur. Customer lifespan estimates how long the relationship continues. Multiply these together, apply your profit margin, and you have a number that changes how you think about that customer.

Consider a customer spending £40 per visit, purchasing twice monthly, staying with you for three years. That's £2,880 in total spending, or £1,008 in profit at a 35% margin. Suddenly this isn't an anonymous transaction, it's a thousand-pound asset walking through your door. How much would you spend to acquire another customer just like them? How much should you invest to keep them from defecting? The answers become obvious once you know the number.

The models grow more sophisticated from here. Early CLV calculations assume static behaviour, but customers evolve. Purchase patterns shift. Frequency changes. Transaction values drift up or down. Advanced approaches use historical transaction patterns to project how individual metrics will change over time. A customer whose transaction frequency has been gradually increasing over the past six months likely has a different future trajectory than one whose frequency has remained flat. Your transaction data captures these trends if you're looking for them.

Predictive models using transaction history have proven particularly effective in non-contractual retail relationships where you can't simply assume customers will renew a subscription. Every visit represents an active choice, and understanding the probability of the next visit based on past behaviour becomes critical for accurate CLV estimation.

The Economics That Follow: CLV Drives CAC

Once you understand what a customer is worth, you know what you can afford to spend to acquire them. This is where transaction intelligence becomes operational rather than just analytical.

Customer Acquisition Cost captures the fully loaded expense of converting a prospect into a paying customer: marketing spend, promotional discounts, sales effort, and everything else deployed to drive that first purchase. If your campaign spent £15,000 and generated 300 new customers, your CAC is £50 per customer.

The CLV:CAC ratio reveals whether those customers will repay your investment. If those newly acquired customers carry a £150 CLV, your ratio sits at 3:1. For every pound spent on acquisition, you're generating three pounds in lifetime profit. Industry consensus suggests targeting ratios between 3:1 and 5:1 for sustainable growth. Below 3:1, acquisition costs eat too deeply into lifetime profitability. Above 5:1 suggests you're under-investing in acquisition when the returns would justify higher spending.

A 1:1 ratio means you're breaking even on a gross basis, which actually represents a loss once operational costs are factored in. You spent £50 to acquire a customer who generates £50 in lifetime profit, but you still need to cover the cost of serving them. This is unsustainable. Ratios below 1:1 indicate value destruction. You're spending more to acquire customers than they'll ever return.

But here's where transaction intelligence enables genuine sophistication: not all customer segments generate the same CLV. Your high-frequency, high-value champions might deliver 8:1 ratios whilst occasional shoppers barely break even. This insight should fundamentally change your acquisition strategy. Double down on channels and tactics that deliver champion-profile customers. Reduce spending on sources that primarily generate low-value segments. Allocate acquisition budgets proportionally to the lifetime value different segments deliver.

Major UK grocery retailers have been applying these principles for years, though they rarely discuss the specifics publicly. When Tesco analyses Clubcard data to understand which customer segments justify premium acquisition costs versus which should be acquired through lower-cost channels, they're making precisely these calculations. Your transaction data enables the same intelligence at your scale.

From Anonymous to Identified: The Next Evolution

For decades, most retail transactions have been fundamentally anonymous. A customer walks in, purchases, pays, and leaves. You capture what they bought and how much they spent, but unless they volunteer to join a loyalty programme, scan a card, or provide their details, you have no idea whether they're a first-time visitor or a regular who comes in every week.

This anonymity has forced retailers into aggregate analysis. You understand patterns across all customers but not individuals. You know Saturday mornings are busy but not whether the same valuable customers visit every week or whether it's constantly new faces. You see seasonal trends in your data but can't identify which specific customers drive them or target them accordingly.

The result is blunt instruments where precision would generate far better returns. Blanket discounts instead of targeted offers. Generic marketing instead of personalised engagement. Acquisition spending that treats all new customers as equally valuable when your transaction intelligence would reveal they're not.

The fundamental limitation has been identification. Without knowing who the customer is, your transaction data remains anonymous and your insights generic. But this limitation is increasingly solvable. Modern payment infrastructure enables customer identification at the point of transaction without requiring customers to present loyalty cards, open apps, or volunteer information. Players in the UK market like Zeal enable card machines to recognise new and returning customers automatically, transforming every anonymous transaction into a known customer interaction.

When your payment systems identify customers at transaction time, everything changes. That anonymous £32.50 purchase becomes "Sarah's fourteenth visit this month, her average basket is £28, and based on her pattern her purchases over the next year are likely worth £850." Your RFM analysis operates on individuals rather than segments. Your CLV predictions inform real-time decisions about which offers to present. Your acquisition costs can be evaluated against actual returning customer value rather than assumptions.

This shift from anonymous to identified transactions represents the next evolution in retail intelligence. You've always captured the data. You've always had the analytical frameworks. What's changing is the ability to connect transactions to individual customers without creating friction. The payment becomes the identification mechanism, and every purchase adds to a customer profile that informs increasingly sophisticated engagement.

Moving Forward

Your transaction data is already the most accurate record of customer behaviour you'll ever have. Every payment represents an actual choice, a revealed preference more reliable than any survey or demographic assumption. The infrastructure to capture this data exists in every modern retail operation. What separates retailers extracting real value from those treating payments as mere revenue mechanisms is analytical commitment and operational follow-through.

The opportunity isn't spending money building new systems from scratch to collect different data. The opportunity is using what you're already collecting to understand customer value, predict future behaviour, make smarter acquisition decisions, and ultimately shift from serving anonymous transactions to building identified, valuable customer relationships.

The data exists. The frameworks are proven. The technology to identify customers at point of transaction is here and continues to advance. The question is how quickly you translate these latent assets into operational advantage before your competitors do the same.

You might also like